Elevate your trading game with TradeUI Pro! Enjoy 2 Months when you go yearly!

Elevate your trading game with TradeUI Pro! Enjoy 2 Months when you go yearly!

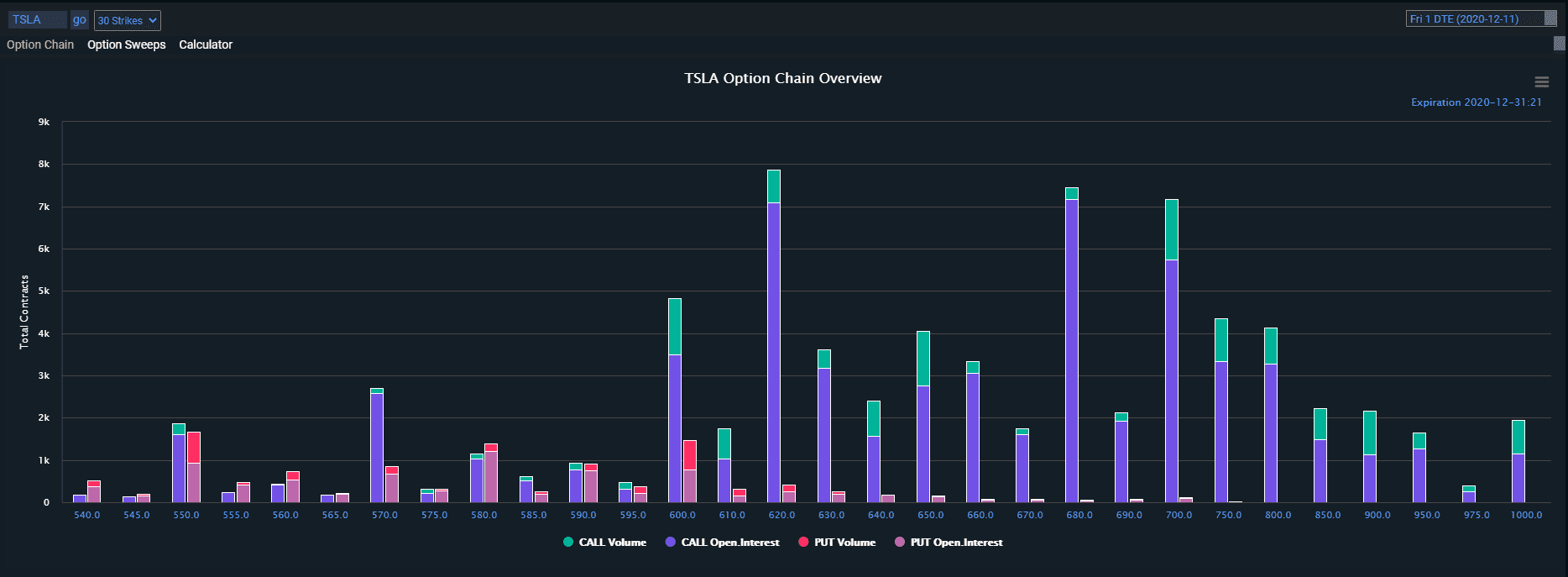

An introduction to Trading with Option Greeks

Options trading can be a complex and sophisticated investment strategy, and one important aspect of this strategy is understanding the “greeks.” These are a set of mathematical calculations that measure different aspects of an options contract and can help traders make more informed decisions about their trades. In this article, we’ll explain what the greeks are and how they can be used in options trading.

The term “greeks” refers to a set of five calculations that are used to measure the sensitivity of an options contract to various market conditions. These calculations are known as delta, gamma, theta, vega, and rho. Each of these greeks measures a different aspect of an options contract, and by understanding how each of these greeks behaves, traders can make more informed decisions about their trades.

Delta measures the sensitivity of an option’s price to a change in the price of the underlying asset. For example, if an option has a delta of 0.50, it means that for every $1 increase in the price of the underlying asset, the option’s price will increase by $0.50. Conversely, if the underlying asset’s price decreases by $1, the option’s price will decrease by $0.50. Delta can be positive or negative, and it can range from 0 to 1 (for call options) or -1 to 0 (for put options).

Gamma measures the rate at which delta changes as the price of the underlying asset changes. In other words, it measures how quickly an option’s delta will change as the price of the underlying asset changes. For example, if an option has a high gamma, it means that its delta will change quickly as the underlying asset’s price changes. This is important for traders to know because it can help them anticipate how their options positions will be affected by changes in the underlying asset’s price.

Theta measures the rate at which an option’s price decays over time. In other words, it measures the option’s time value, or how much of its value is derived from the amount of time remaining until expiration. For example, if an option has a theta of -0.10, it means that its price will decrease by $0.10 per day as the expiration date approaches. Theta can be positive or negative, and it is generally higher for options with shorter time to expiration.

Vega measures the sensitivity of an option’s price to a change in the volatility of the underlying asset. In other words, it measures how much an option’s price will change in response to a change in the underlying asset’s volatility. For example, if an option has a vega of 0.50, it means that for every 1% increase in the underlying asset’s volatility, the option’s price will increase by $0.50. Vega can be positive or negative, and it is generally higher for options with longer time to expiration.

Rho measures the sensitivity of an option’s price to a change in the risk-free interest rate. In other words, it measures how much an option’s price will change in response to a change in the risk-free interest rate. For example, if an option has a rho of 0.10, it means that for every 1% increase in the risk-free interest rate, the option’s price will increase by $0.10. Rho can be positive or negative, and it is generally higher for options with longer time to expiration.

So, how can traders use the greeks in their options trading strategies? By understanding how each of these greeks behaves, traders can better anticipate how their options positions will be affected by changes in the underlying asset’s price, volatility, and interest rates.