Elevate your trading game with TradeUI Pro! Enjoy 2 Months when you go yearly!

Elevate your trading game with TradeUI Pro! Enjoy 2 Months when you go yearly!

In options trading, one party has to buy an option, and the other has to sell, and that party can be a brokerage dealer, derivatives shop, or market maker. We can say options trading is a zero-sum game.

Flattening the Risk:

Delta of the stocks calls move with the underlying instrument, and it goes up the Delta will also move up. Before the move, dealers who were initially Delta hedging purely short the stock when it moves high, and to flatten the risk or hedge up, they have to buy more shares.

Delta hedging:

Large institutions or hedge funds put big call trades as they are having a bet on an expected near move. When a stock moves up, the dealers have to re-hedge when that move plays out. That’s how they are underlining “big wise-guy trades” or “smart money trades.”

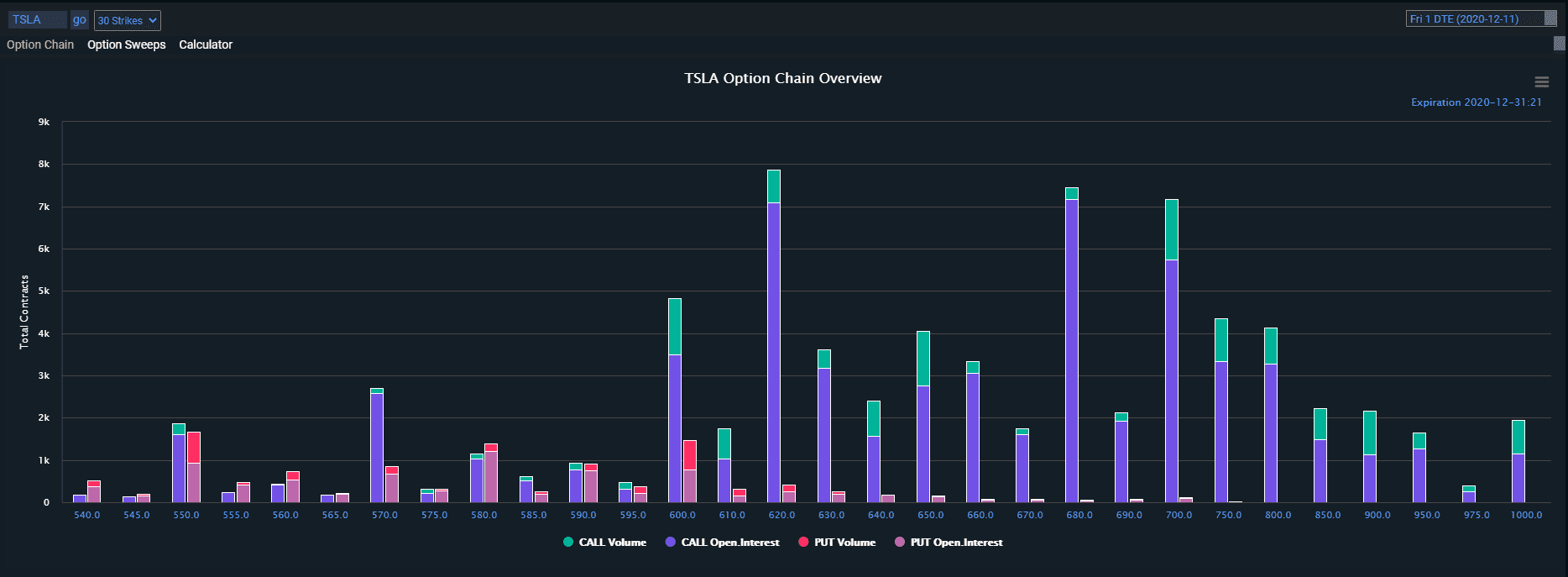

Brokerage firms’ option trading desks trade almost all the large option trades. Trading five thousand plus stock options contracts at a clip will affect the price of options so that there will be no liquidity in most stock options.

Delta neutral hedging example:

Let take an example of Delta neutral that a trader at hedge funds goes to brokerage firm options trading desk and asks to buy $AAPL May 45 calls or for more significant trades, and the trader will say “give me a menu.” The screen on the trading desk will be showing 40c/45c. The desk would respond, one thousand at 45c, three thousand at 50c, and five thousand at 60c.

If the trader says “five thousand at 60c,” and now the brokerage firm is naked short the calls.

Now the trading desk will see;

- The trading desk will see that, if they have the stock or it supports their entire risk to keep, maybe they keep the stock.

- The trading desk will see that, is there little liquidity in the screen market? They also recognize that without moving the market, are they get out of the risk?

- The trading desk will try to buy more options to hedge themselves by buying at the higher strike price or creating synthetic calls and buying both puts and stocks. But this is a particular way and affects the possible gains.

- If the trading desk buys the sum of stock of the option delta, let’s say $AAPL May 45 calls are ~ 0.25 delta, so they have to buy 125,000 of stock.

One hundred twenty-five thousand shares effectively become short until the stock moves up 5%, and Delta of calls goes to 0.5 from 0.25, and the dealer has to buy 125,000 more stocks for delta hedging with stocks.

The above example is an easy one but visualizes a stock in a day trades 300k, and the dealer becomes short 5k calls, a 5% move turn into 15% move, and the dealer will use delta neutral strategy. Buying more stock will increase the buying pressure, and the stock goes higher.

Day-traders:

Not one person wants to short or sell a long position when the stock moves quickly for no reason. Traders think that some positive news is coming out, and large call buying improves its integrity. Some day-traders are hoping to gain profits from anything that is moving, and this eliminates the liquidity, and buyers start buying the stocks, then stock move higher.